Transfer pricing is not an exact science

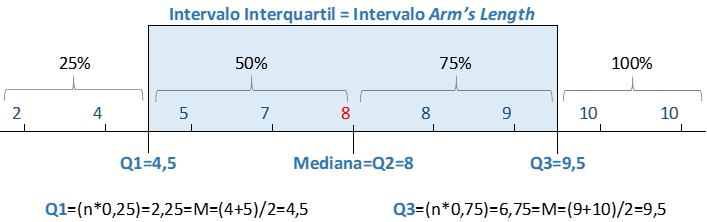

Chapter II of the OECD Guidelines (TPG) presents the five transfer pricing methods, divided into two groups: Traditional Transaction-Based Methods and Transactional Profit-Based Methods. The purpose of these methods is to verify whether transactions between companies in the same economic group comply with the Arm's Length principle. Traditional transaction-based methods are considered the most direct means of verifying whether the conditions of commercial and financial relations between associated companies are "arm's length". Whenever it is possible to apply a traditional transaction-based method and a transactional profit-based method equally reliably, the traditional transaction-based method is preferable to the transactional profit-based method. The selection of a transfer pricing method always seeks to identify the most appropriate method for each specific case. This does not mean that all transfer pricing methods must be analyzed or tested in each case in order to select the most appropriate method. There is no hierarchy in the selection of methods, but the method chosen should be the one that best meets the "Arm's Length" principle. Good practice recommends that methods not chosen should be listed and the reason for not being chosen justified. However, the preferred method, considered to be the one that best meets the market value principle, is the Comparable Independent Price (CUP) method. What is more important than choosing a calculation method is admitting that Transfer Pricing is not an exact science, and that there will hardly ever be identical and comparable operations. The OECD recognizes that Transfer Pricing is not an exact science. There will be many occasions when the application of the most appropriate method or methods will produce equally reliable results. In this sense, the OECD Guidelines suggest establishing a range of acceptable values: the Arm's Length Interval or Interquartile Range. This range identifies a series of reliable and acceptable comparisons. The Interval Arm’s Length suggests excluding samples at the two extremes: 25% of the lowest values and 25% of the highest values. These values may possibly have been influenced by factors that cannot be adjusted for comparability. The central range of the sample of values represents the valid values. In this range of values, the Arm’s Length. The center of the sample corresponds to the Median of the Data (Q2). The positions Q1=Q2-25% and Q3=Q2+25% represent the limits of the interval.  The Brazilian rules sought to incorporate this concept through the Margin of Divergence. But the difference in concepts is notorious. Domestic legislation calculates the ideal price and accepts a small variation. The OECD concept establishes a range of valid values. In order to identify comparable operations, the OECD guidelines established the concept of Comparability Analysis, which we will cover in our next article. Until then! Demetrio Barbosa

The Brazilian rules sought to incorporate this concept through the Margin of Divergence. But the difference in concepts is notorious. Domestic legislation calculates the ideal price and accepts a small variation. The OECD concept establishes a range of valid values. In order to identify comparable operations, the OECD guidelines established the concept of Comparability Analysis, which we will cover in our next article. Until then! Demetrio Barbosa

demetrio@tpbluemind.com

To share