Brazil: Provisional Measure to align transfer pricing rules with OECD Transfer Pricing Guidelines

At the end of 2022, the Brazilian government published Provisional Measure (MP) 1152/22 to align Brazil's transfer pricing rules with the OECD Transfer Pricing Guidelines. The provisional measure must be approved for conversion into law by the Brazilian parliament (congress and senate) within 120 days. Although it is not certain, it is expected that the new government and the newly elected parliament will support the approval of the provisional measure (end of April/23).

Following the enactment of the new law, the Brazilian Federal Revenue Service is expected to issue a Normative Instruction to regulate the new law and provide guidance on its application. Although it is already possible to assess the new consequences of the Provisional Measure, only once the new law and regulations have been issued will Brazilian taxpayers be able to properly assess the effects and consequences. For calendar year 2023, Brazilian taxpayers can choose between the current transfer pricing rules and the new OECD-based rules. Due to the lack of regulation, Brazilian taxpayers will probably face tough hurdles in assessing the consequences of the new rules.

From January 1, 2024, if approved by the Brazilian parliament, the new OECD-based rules will be mandatory.

Overview of the proposed changes

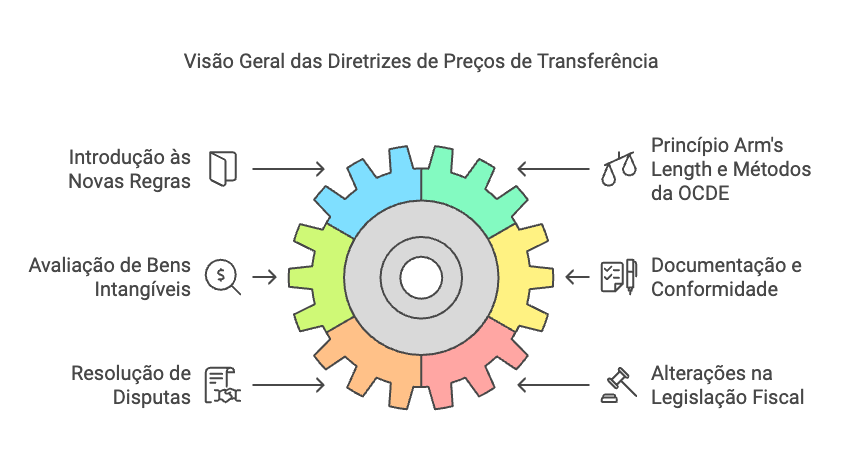

The Provisional Measure outlines the new regulation in six chapters:

Chapter I: general introduction to the new rules that will be reflected in the calculation of IRPJ and CSLL.

Chapter II: presents the Arm's Length Principle, the OECD Transfer Pricing Methods, including the Transactional Net Margin Method and the Profit Split Method, and the comparability analysis.

Chapter III: introduces concepts for valuing intangible assets, intra-group services, cost contribution agreements and financial transactions.

Chapter IV: provides general guidance on the expected Transfer Pricing documentation and penalties in the event of non-compliance.

Chapter V: provides guidance on administrative approaches to avoiding and resolving transfer pricing disputes.

Chapter VI: Amends tax legislation that contradicts the proposed transfer pricing rules.

In view of the Draft of the new Brazilian Transfer Pricing rules, it is worth highlighting:

- Financial transactions, including insurance and loan guarantees, should be subject to transfer pricing rules.

- The transfer pricing method selected must be "the most appropriate method" to meet the arm's length pricing principle.

- The Net Transaction Margin and Transactional Profit Split methods introduced.

- Comparability analysis, including analysis of functions, risks and assets.

- Intangible assets should be a critical area, requiring functional DEMPE analysis (Development, Maintenance, Enhancement, Protection and Exploitation).

- Corporate restructuring must be reviewed from the perspective of the arm's length principle. Active M&A should be a critical area.

- Different types of transfer pricing adjustments (spontaneous by the taxpayer, imposed by the Tax Authority, end of the calendar year, during the calendar year) should be possible. This should be a critical area because, in order to avoid double taxation, taxpayers must be able to adjust profits before the end of the year between companies in different jurisdictions.

- Possibility of specific consultation on the matter and mutual agreement procedure (MAP).

We believe that MP 1152/22 will most likely be approved by Congress by the end of April/23. It is possible that the MP will receive amendments and therefore it would be a good approach to wait for the legislative process to be concluded in order to have a better view of the scenario. In addition, as a final step, the Brazilian tax authorities must regulate the application of the new law by means of a Normative Instruction. Although it is possible to assess the scenario preliminarily, once the new law has been enacted and regulated, Brazilian taxpayers should be able to accurately assess the effects and consequences.

f you have any questions, we are ready to help you.

Bluemind | www.tpbluemind.com

Demetrio Barbosa | demetrio@tpbluemind.com

Juliana Campos | juliana.campos@tpbluemind.com

To share