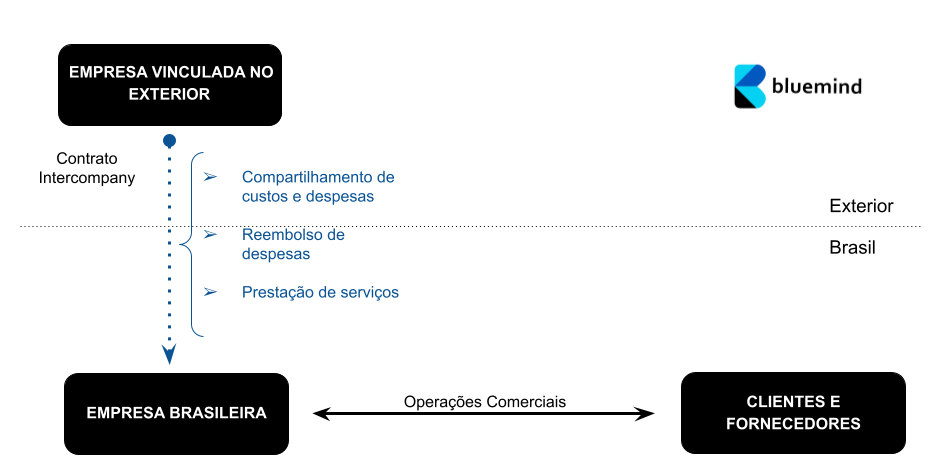

Intercompany services

Most of the services contracted from group companies abroad result in points of contention between the management of the Brazilian company and other agents: the service providers, the Internal Revenue Service, auditors, consultants and lawyers.

Just to make it easier to read the scenario, I will classify these services into:

- Specific, when it originates from a demand and could also be contracted from a third party. In this scenario, the scope of the service is previously identified, a price is agreed, a product (tangible or intangible) must be delivered and a benefit must be derived.

- Corporate: one or more companies in the same economic group carry out activities that produce advantages and benefits for themselves and other companies in the group that would be difficult to contract from third parties. The service is made available, but not necessarily used.

The first step is the general rule of deductibility (art. 299 of the RIR). In this sense, the amounts contracted will only be deductible when:

- They correspond to expenses necessary for the activity and maintenance of the respective source of production;

- Are paid or incurred to carry out the operations required in the activity;

- They are usual or normal in the type of transactions, operations or activities.

The second stage corresponds to proving that the adjusted and contracted price complies with Brazilian Transfer Pricing rules (Law 9.430/96, art. 18). In order to comply with this commandment, it will be necessary to choose one of the methods available in the aforementioned law.

Among the options, the Compared Independent Prices (CIP) and Cost of Production plus Profit Margin (CPL) methods depend on comparable operations with third parties and information on the cost of services abroad. These methods have limited applicability, since the information required is hardly available to the Brazilian company.

The last method, Resale Price minus Profit (PRL), with the changes introduced at the end of 2012, has become an excellent alternative. This is because its calculation requires information available in the Brazilian company's accounting and tax records.

The use of the PRL method requires certain precautions, including (i) identifying the direct or indirect revenue produced or induced by the imported service and (ii) incorporating the expense of the service into the cost of the "sale".

Once the deductibility and transfer pricing stages have been overcome, the third stage to overcome is taxation. And the list is long: IR Fonte (15% or 25%), CIDE (10%), PIS Import (1.65%), COFINS (7.6%), ISS (2% to 5%) and IOF (0.38%).

The import of services and its tax consequences have been a recurring theme for the Brazilian Federal Revenue Service (RFB). In my studies, I have selected the consultation solutions listed below for closer reading:

- Consultation Solution 008 - Cosit - 01/11/2012

- Consultation Solution 013 - Cosit - 23/09/2013

- Answer to Advance Tax Ruling Request 378 - Cosit - 23/08/2017

- Answer to Advance Tax Ruling Request 021 - Cosit - 21/09/2017

- Consultation Solution 094 - Cosit - 25/03/2019

My attention was drawn to those queries in which the taxpayer argued that the transaction should not be taxed, since it was a reimbursement of a cost or expense. As such, it could not be taxed as a service transaction. The RFB dismissed these queries, arguing that:

- There was no mutual benefit between the participating companies in the contract;

- The service provider only carries out the service and does not obtain any advantage other than the amount received.

Service and cost-sharing contracts need a lot of attention. Highlights:

- Contract formalization and periodic reviews of terms and conditions.

- Breakdown of services and reimbursements.

- Forecast deliverables.

- Objective remuneration rule.

- Charging for services on presentation of deliverables.

I hope the content has been useful and I'm happy to talk about your practical case.

Cheers!

Bluemind

Demetrio Barbosa

demetrio@tpbluemind.com

To share